Dollar-Cost Averaging Revisited

When we look at the world of investing today, compared to, let’s say 30 years ago, the advancements in technology have been truly amazing. We have information at our fingertips 24 hours a day, unbelievable trading capabilities, exchange traded funds, etc. When I first started, mutual funds published their prices in their prospectus once per year. Combining the old with the new, and as it relates to investing strategy itself, there are a few tried and true things that, along the way, have become timeless building blocks for successful wealth management. Buy low and sell high, diversify, re-invest dividends, time in the market, not timing the market, etc. One tool we wish to focus on in this article is something called dollar-cost averaging.

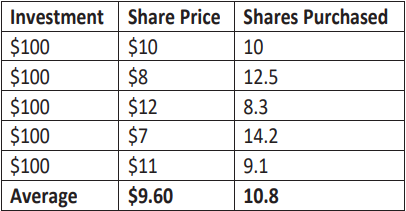

So, what is dollar-cost averaging? It is simply a process of investing a set amount of money at regular intervals, attempting to take advantage of price fluctuations in the market. For example, as the chart below illustrates, we take a set amount of $100 per month and invest it in our hypothetical fund. While the amount we put in each month is the same, the share price and amount of shares we purchase fluctuates. When prices are lower, we accumulate more shares, and when they are higher, we get less. However, over time we hope that our average purchase price is lower, and we gain the opportunity to own more shares.

While dollar-cost averaging offers the potential to hopefully own more shares at a lower price over time, we believe there are additional benefits that are just as important. First, it reduces timing risk by setting automatic investment intervals. Second, it builds discipline into our lives and makes investing a consistent thing. Finally, it takes the emotion out of it and puts a solid plan in place for future wealth creation. These are all good things that provide the opportunity for long-term financial success.

Investing involves risk. No investment strategy can guarantee positive results. Loss, including loss of principal, may occur. Material discussed is meant to provide general information and it is not to be construed as specific investment, tax or legal advice. Keep in mind that current and historical facts may not be indicative of future results. Diversification is an investment strategy that can help manage risk within a portfolio, but it does not guarantee profits or protect against loss in declining markets.

This content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. (C) Twenty Over Ten